It looked like it should have been a good week for the Rand...

...but markets had other ideas.

By Tuesday, Stats SA had confirmed Q4 unemployment dropped to the lowest in five years. By Wednesday, inflation came in at just 3.5% year-on-year. The IMF published a broadly positive assessment of SA's economy on Thursday...

And through it all, there were 240+ days without a single hour of load shedding on record.

Yet the Rand opened the week at R15.94...

...and by Thursday's close had drifted to R16.14.

The culprit? A cocktail of global pressures — a hawkish FOMC signal, Iranian tensions rattling oil markets, and a US tariff saga that produced more twists on a single Friday than most weeks manage all week.

Here's how it all played out...

Key Moments (16-20 February 2026)

These were some of the major headlines and events over the past five days:

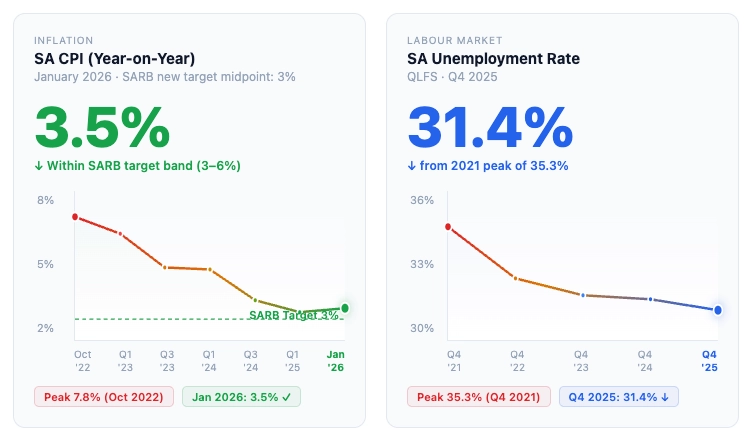

📊 SA Unemployment Falls to 31.4%: Q4 2025 QLFS shows five-year low — 172,000 fewer unemployed; 17.1 million employed (released 17 Feb)

🌡️ SA CPI Cools to 3.5%: January 2026 inflation eases from 3.6% — firmly within SARB's new 3% target framework (released 18 Feb)

🏦 SARB Floats Prime Rate Reform: Reserve Bank launches consultation on replacing the prime lending rate with the repo rate — transparency push, no immediate rate changes (16 Feb)

🌍 IMF Endorses SA's Recovery Path: "Sound institutions, flexible exchange rate, credible monetary policy" — growth forecast 1.4% in 2026 (19 Feb)

🇺🇸 FOMC Minutes: Rates on Hold — Longer: Fed policymakers signal inflation still too sticky for cuts — DXY pushed toward one-month highs mid-week

🛢️ Iran Tensions Drive Oil to $71: US military buildup, Strait of Hormuz threats, and a 10-day deadline for talks — Brent crude spikes, EM risk-off pressure builds

⚖️ Supreme Court Kills Trump Tariffs — Then He Announces New Ones: 6-3 ruling strikes down IEEPA tariffs on Friday; Trump announces 10% global tariff within hours

Monday: Quiet Start, Structural News 🟢

Monday opened quietly on the Rand front...

...but in Pretoria, the Reserve Bank made a structural announcement that will affect every borrower in the country — eventually.

The SARB published a consultation paper proposing to abolish the prime lending rate — the number that's been the reference point for home loans, business credit, and vehicle finance for decades — and replace it with the repo rate directly. The argument: more transparency, a clearer link between SARB decisions and actual lending costs.

For context, prime currently sits at 10.25%, exactly 350 basis points above the repo rate of 6.75%. The reform wouldn't change that gap — but it would change how it's disclosed and referenced.

Timeline? No earlier than 2027. (That's a very South African timeline — but the direction is right.) But the consultation is open now.

For the Rand, it was a non-event on the day — with USDZAR confined to an 11.8-cent range, ending just 3.9c weaker at R15.982. The calmest day of the week.

Tuesday: Jobs Data Lands 🟡

Tuesday delivered the week's most consequential local data...

...and it was better than many expected.

Stats SA released the Q4 2025 Quarterly Labour Force Survey: South Africa's official unemployment rate dropped to 31.4% — down from 31.9% in Q3. The lowest reading in five years. 172,000 fewer unemployed people. Employment up 44,000 to 17.1 million.

The caveats were real: trade (-98,000), manufacturing (-61,000) and mining (-5,000) shed jobs. Youth unemployment for 15-34 year-olds edged up to 43.8%. Eastern Cape remained the hardest-hit province. And 5.8 million young people are still without work.

But the headline trend? Moving in the right direction.

The Rand should have liked this...

...and it opened stronger, testing R15.923 on the session low. But by close, global risk-off sentiment had pushed USDZAR back to R16.017 — up 6.1c on the day, in a 19.1c range that included the week's strongest and some of its weakest levels.

The pull factor? Global. Not local.

Wednesday: Inflation Confirms, Ambassador Arrives 🟡

Wednesday brought two very different pieces of news...

...one from Stats SA, one from OR Tambo International Airport.

First, the data: January 2026 CPI came in at 3.5% year-on-year, down from 3.6% in December. Food and non-alcoholic beverage inflation eased. Transport costs softened. The reading sits comfortably within the SARB's new lower inflation target framework — the lowest level since the reserve bank adopted its 3% point target.

For context: twelve months ago, South Africa's inflation was running above 5%. The progress has been significant.

Then the other news: Leo Brent Bozell III, Trump's pick for US Ambassador to South Africa, arrived in Pretoria. Founder of the Media Research Center, Bozell has been openly critical of SA's foreign policy alignment — particularly its ties to Russia, China and Iran. His appointment signals the US intends to push harder on the issues that have strained relations — the ICJ case, SA's non-aligned stance, land reform.

He still needs to present credentials to President Ramaphosa. The diplomatic chapter hasn't formally opened yet...

...but the temperature in SA-US relations was already clear.

On markets, USDZAR ended 2.4c weaker at R16.064 — the week's smallest daily move.

And in other news...

US-Iran Tensions Build 🛢️

The US military buildup in the Middle East continued to escalate through the week. Two carrier strike groups positioned near the Strait of Hormuz. Iranian gunboats had seized tankers in early February. By Wednesday, negotiations appeared stalled — with military action openly discussed as a live option.

Oil responded: Brent crude pushed toward $71/barrel, its highest level in six months. Risk-off sentiment spilled into emerging markets — the Rand among them.

Gold Breaks Through $5,000 🥇

Despite a broader risk-off tone in EM currencies, gold surged through the week — opening near $4,900/oz and breaking above $5,000 by Friday. The persistent safe-haven bid continued to widen the gap between gold and Bitcoin: BTC remained range-bound between $65K and $73K, down nearly 50% from its October 2025 peak.

The "digital gold" narrative took another hit.

DXY Edges Higher 💵

The US Dollar Index climbed toward one-month highs mid-week, hovering around 97.7-98.5. The driver? Anticipation of Thursday's FOMC Minutes release, combined with hawkish Fed commentary — policymakers broadly signalling no cuts in the near term given sticky core PCE inflation (3% in December).

For EM currencies — the Rand included — a stronger dollar mid-week added to the headwinds.

To get back to the Rand...

Thursday: FOMC Minutes Bite 🔴

Thursday was the week's worst session for the Rand...

...and the Fed was the primary driver.

FOMC Minutes from January's meeting confirmed what the market had been quietly fearing: the Federal Reserve is in no hurry. Policymakers flagged persistent inflation, uncertainty around tariff pass-through, and a labour market that's cooling — but not fast enough to justify cuts.

With Trump simultaneously pushing for lower rates and the Supreme Court weighing in on tariff powers, the environment was unusually uncertain.

USDZAR traded in a 20-cent range — the widest of the week — touching a high of R16.223, the weakest level for the Rand all week. By close, some of the move had been given back, settling at R16.145...

...but the direction was clear.

On the same day, the IMF published its latest country analysis on South Africa...

...and the assessment was broadly constructive. Despite the challenging global environment, SA's growth picked up in 2025. Inflation fell. Bond yields narrowed. Growth is projected at 1.4% in 2026, rising toward 1.8% medium-term.

The IMF endorsed SA's new 3% inflation target and praised its "sound institutions" and "credible monetary policy framework."

(Yes, the IMF actually wrote that...About South Africa...This week.)

The caveats were significant: debt is projected to rise toward 81% of GDP without fiscal discipline. The Budget Speech — just one week away, on 25 February — needs to deliver a credible primary surplus path.

Two steps forward on the fundamentals...

...one step back on the currency, as global risk dominated.

Friday: The Supreme Court, New Tariffs, and a 12-Cent Reversal 🟢

Then came Friday...

...and it delivered enough news for an entire week.

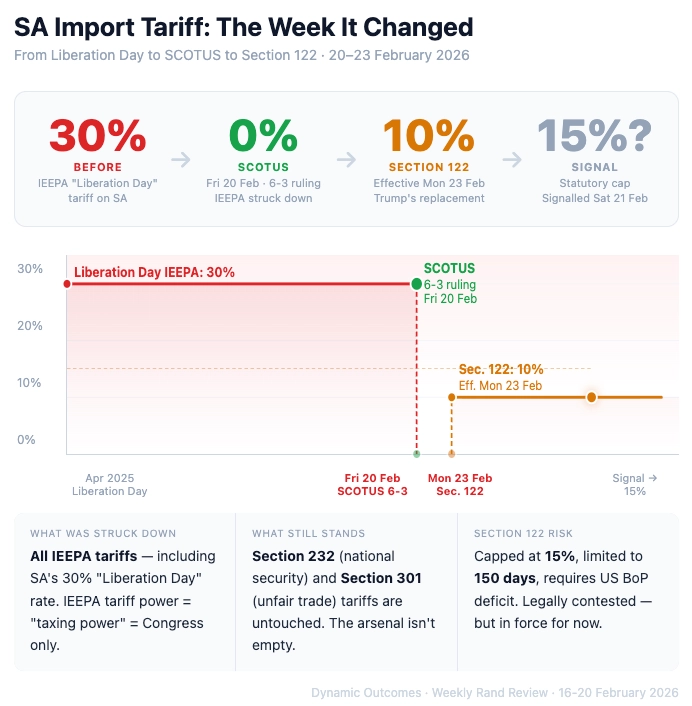

In Washington, the US Supreme Court handed down a landmark 6-3 ruling in Learning Resources, Inc. v. Trump: Trump's use of the International Emergency Economic Powers Act (IEEPA) to impose tariffs was unconstitutional.

The Court held that tariff power is "very clearly a branch of the taxing power" — reserved for Congress, not the President. The ruling was broad: it invalidated all IEEPA-based tariffs, including the 30% "Liberation Day" tariff that had been applied to South Africa since last year...

...opening up potential refunds for importers who overpaid are now on the table.

Markets reacted immediately: the DXY dropped. Risk sentiment improved. Equities bounced. Emerging market currencies — including the Rand — strengthened hard.

USDZAR dropped from its opening high of R16.194 toward R15.984 on the day's low — a 21-cent intraday range, the widest of the week.

But Trump didn't wait long to respond...

...within hours of the ruling, he announced a new 10% global tariff under Section 122 of the Trade Act of 1974 — a statute that allows the President to impose temporary import surcharges to address balance-of-payments deficits.

The legal ground here is also contested: Section 122 is capped at 15%, limited to 150 days, and requires the US to have a "large and serious" international payments deficit...

...of course you have "trade experts" saying these conditions don't exist under a floating exchange rate - but they fail to actually address the decades-long problem that Trump is trying to fix!

By Saturday, Trump had already signalled a raise to 15% — the statutory maximum. The legal fight isn't over. The tariffs, for now, aren't either.

Markets reversed some of the move. The DXY recovered. The Rand gave back ground.

One footnote the headlines missed: the SCOTUS ruling didn't disarm Trump's entire tariff arsenal. Section 232 (national security tariffs) and Section 301 (USTR unfair trade practices) — both heavily used in his first term and renewed in the second — were untouched by the ruling and remain in force.

Bottomline: The legal victory for importers on IEEPA is real. But it didn't demolish the architecture.

And there's a broader context worth holding. The ruling may look like a clean win for free trade — but Trump's core trade grievance isn't simply invented.

As we spelt out in this month's Market Demystifyer, the USA has run persistent trade deficits for decades under WTO "Most Favoured Nation" rules that often gave trading partners lower US tariffs than the US received in return.

Whether or not IEEPA was the right legal tool, the underlying imbalance is real — and it's the political fuel behind every tariff headline coming out of Washington.

This isn't a story that ends with a court ruling. It ends with commonsense levelling of the playing field. And that is Trump's end game.

But for the Rand, the net result was that the USDZAR closed at R16.039 — down 11.9c from the open, but well off the day's strongest levels. A partial recovery at week's end, leaving the week's story as: four days of creeping weakness, then Friday's geopolitical whiplash.

Volatility and Risk Analysis

Here's how the volatility played out:

• Open to Close Move: R15.943 to R16.039 = +9.6c weaker (+0.60%)

• Average Daily Range: ~17.5c

- Risk per $1 Million Exposure: R175,000

• Maximum Single-Day Move: 21.1c on Friday 20 Feb

- Risk per $1 Million Exposure: R211,000

• Weekly Range: 34.2c (R15.881 to R16.223)

- Risk per $1 Million Exposure: R342,000

• Weekly Low (Rand Strongest): R15.881 on Monday

• Weekly High (Rand Weakest): R16.223 on Thursday

For a business with $1 million in monthly USD obligations, this week's average daily range represented approximately R175,000 in exposure per day — just from intraday movement. The Thursday-Friday sequence alone (41.1c combined range across two days) carried over R411,000 in swing risk.

The week's pattern — grinding weakness Monday-Thursday, sharp Friday reversal — is a reminder that currency timing isn't about picking a direction. It's about managing the range.

The Week Ahead (23-27 February 2026)

SA: Budget Speech — Finance Minister Godongwana tables 2026 Budget in Parliament, Wednesday 25 Feb at 14:00

US: Durable Goods Orders (Wed), PCE Inflation — the Fed's preferred measure (Fri)

Global: Iran 10-day deadline (Trump stated decision on military action by then); AGOA tariff situation — IEEPA struck down (30% SA tariff), replaced by 10% Section 122 effective 23 Feb, signalling 15% raise

What to Watch

The week's centrepiece for SA: South Africa's Budget Speech on Wednesday, 25 February.

Finance Minister Enoch Godongwana 2026 Budget will be watched closely (especially by the IMF) for the credibility of the path to a primary surplus, treatment of debt (currently projected at ~77.9% of GDP), any changes to personal or corporate tax rates, and direction on SOE funding and the public sector wage bill.

And then, of course, Trump's State of the Union address on Tuesday is the week's other centrepiece. Markets will be watching for any tariff announcements — particularly whether Section 122 remains at 10% or moves to the signalled 15% — as well as any commentary on Iran, the Fed, or fiscal policy.

After a week in which a Supreme Court ruling failed to end the tariff story, the SOTU is the next venue where Trump can signal direction.

To round off, it was a week where South Africa's own story was genuinely good...

...but the Rand moved to a different beat.

Unemployment falling. Inflation cooling. IMF endorsing. 240+ days of lights on. All of it real, all of it positive. Yet four of five days saw the Rand weaken — pulled by Iran, pulled by the Fed, pulled by the daily noise of a world in flux.

That's the nature of a small, open economy and a freely traded currency. The fundamentals matter. They just don't always win on a Tuesday. (Ask anyone who traded the Rand on Tuesday.)

Next week, we get the Budget Speech — and one of the clearest statements yet on whether SA's fiscal story matches the narrative. We'll have full coverage in next week's Review.

To your success~

James Paynter

P.S. We've been doing this for over 20 years. In that time, we've tracked thousands of forecasts — and if you'd asked me whether our calls were accurate, I could give you an honest answer, but not an accurate documented one...

...no objective record — just instinct and memory.

That's changed. We've built a dedicated AI-driven track record model that captures our forecasts and scores them against actual market outcomes — in real time, without any curation. No cherry-picking the wins. No quietly forgetting the misses. The full record, as it happened.

I've wanted something like this for a long time. Getting it right took longer than expected. But it's done — and we'll be publishing the first full report shortly.

If you've ever wondered how accurate our forecasting actually is, you'll soon have the data to judge for yourself.

"Good local data doesn't always save you...

...when the world has other plans.

Manage your timing of your exposures...

...not the direction."

...and understand what's really moving markets

Here's what you'll discover:

- How the cycles work — and what to do when the wind changes

- Why most forex strategies fail (and it's not what you think)

- How to recognise turning points BEFORE they happen

- Why the Fed doesn't control interest rates

Plus much more...

No jargon. No predictions pulled from thin air. Just cycle structure + sentiment data + what it means for YOUR positioning. As well as simple layman's explanation of complex economics, and what this means for you.

Flying Blind Is Costly

This week proved once again that markets move in cycles, not linear economist logic.

While mainstream analysts were celebrating Tuesday's Dow record, our forecast system was already signaling the Rand would push through R17 before reversing...

...and it delivered, hitting R16.95 - dead centre of our predicted 17.08-16.89 range...

...before losing 25 cents in a classic reversal.

That's not luck.

That's systematic forecasting based on a combination of sentiment cycles, Elliott Wave, momentum, wave ratios & relationship studies, momentum and supply & demand...

...the same system that's kept us and our clients ahead of the curve for years.

Want to see where the Rand is headed next?

To get a look at the latest forecasts, use the link below:

Click here to view the latest forecasts

If you have any questions or feedback, please leave them below.

To your success~

James Paynter

Got any questions? Here's what to do:

2. Call us on 087 551 2848

3. Chat with us using our Whatsapp chat

P.P.S. Want some insights as to where the Rand is likely to move - enabling you to make educated and informed decisions - ahead of time?

Take our Rand Forecasting service for a test-drive using the link below

No charge. No card. All yours to try out for 14 days.